You will probably hardly find much case law on space disputes in the public domain since most of them are settled in arbitration and are therefore confidential. Nevertheless, sometimes case files become available to the public. Frankly, not all space disputes are genuinely “space” as they usually arise from contracts, intellectual property, torts, etc. However, that does not make them less interesting. Today we will discuss five such notable space disputes as part of our Space Law practice.

Our expertise in Space Law

From satellite operators and launch service providers to new-age space tourism companies — we serve a range of clients in the space industry, offering comprehensive services in regulatory compliance, intellectual property, contracts, and dispute resolution.

Learn more about our experience in Space Law1. Rentals for Asteroid Parking

Let’s start with a case that deserves special attention since it addresses property rights in space. In 2004, the US Federal Courts first heard a case in which the right of ownership over an asteroid was litigated (Nemitz v. NASA case).

The plaintiff, Gregory Nemitz, claimed the asteroid Eros as his property and sought to charge NASA an annual rent of $0.20 as NASA had orbited its NEAR Shoemaker on the asteroid in 2000. Since rent was claimed for 100 years ahead, the amount claimed was only $20.

Of course, NASA and the US State Department were in no hurry to pay anyone even that paltry sum, so they just showed Nemitz the door and, based on their own interpretation of the Outer Space Treaty (1967), denied his claims.

The case was then referred to the Federal Court. On November 6, 2003, Nemitz asked the jury to decide the issue of space ownership and set the first precedent in space property law. Over the next several months, the prosecutor filed motions to extend the time for response. Thereafter, on January 28, 2004, the prosecutor’s office declared that the plaintiff had not presented sufficient evidence to support his case. In response, the plaintiff argued that the part of the claim concerning contractual breach was indeed without merit. However, the other part, relating to private property rights in space and the interpretation of the Outer Space Treaty, was still at issue and was left for the court to consider.

Finally, the court held that Nemitz failed to substantiate his legally enforceable property interest in ownership over the asteroid.

It is worth noting, however, that in this case, the court did not decide that there are no property rights in space or that individuals cannot acquire those in respect of celestial bodies. Rather, the court held that none of the grounds on which Nemitz relied upon had established any property rights to the Eros asteroid.

2. Deposit Refund for a Failed Cruise Around the Moon

Harald McPike, an Austrian businessman and fortune seeker, filed a lawsuit against Space Adventures in May 2017 demanding repayment of a $7 million deposit. He had paid this amount as an advance under the contract that was to provide him, as a space tourist, a seat on a Soyuz spacecraft. The total price per seat was $150 million. The mission was supposed to fly around the moon. In his lawsuit, McPike also claimed other damages.

McPike alleged in his complaint that in July 2012, he approached Space Adventures regarding the opportunity to participate in a mission around the moon, which the company had been pursuing for several years. In March 2013, he signed a contract and made a deposit of $7 million toward the total $150 million, anticipating that the mission would take place within the next 6 years.

A year after the contract was signed, McPike was supposed to make a second payment of $8 million, but he delayed it as mission preparations slowed. In particular, there was still a lack of information from the Russian companies and agencies that were to implement the mission. In 2015, after McPike failed to make the second payment, Space Adventures terminated the contract and retained the already paid deposit.

According to McPike’s lawsuit, he later contacted the Russian space agency Roscosmos directly, which informed him that despite a signed contract, there was no official relationship between the agency and Space Adventures for a near-lunar mission. This mission, like a number of other future projects, was only at the “preliminary planning stage.”

McPike filed a lawsuit on several grounds, including breach of contract, fraud, and breach of contractual warranty under the laws of Virginia, where Space Adventures was based. Some of these theories, including the unjust enrichment, were dismissed by the court in late 2017. The judge also dismissed motions for summary judgment from both plaintiff and defendant, declaring that the matter of whether there had been a breach of contractual warranties between the company and McPike must be tried to a jury.

The judge, however, was receptive to McPike’s argument that there had been a breach of warranty due to the lack of a formal agreement between Space Adventures and Roscosmos for the near-lunar mission. In particular, the judge stated that the plaintiff was correct that the separate written agreements and memoranda of understanding between Space Adventures and Roscosmos did not demonstrate that the company had the right to provide a near-lunar mission. Nevertheless, the judge also added that the pre-trial statements of the company’s representatives demonstrated that the company could have been authorized for this mission by virtue of a number of written and oral agreements.

The case was referred to a jury trial, which was scheduled for April 9, 2018. However, two weeks later, the parties reached a settlement agreement. What they agreed upon is unclear. It is only known that each party has agreed to pay their own litigation costs, but they have made no comment on the fate of the $7 million deposit.

3. Royalty and Satellite Services

This case is known as Asia Satellite Telecommunications Co. Ltd. v. Director of Income Tax. In this case, an Asian satellite operator provided two Hong Kong-owned satellites for retransmission to Indian TV operators. Both satellites were placed into geostationary orbit, they were not within the Indian orbital intervals allocated by the International Telecommunication Union and were not positioned over Indian airspace.

The satellite coverage area extended to several countries, including India. The satellite operator had therefore agreed to provide satellite retransmission services to TV companies for broadcasting their programs to the Indian audience. During the hearing, the Delhi High Court examined whether the income of a foreign satellite company received for the transmission of TV signals from outside India could be deemed as royalties subject to tax in India.

The Hong Kong company’s only activities on Earth were limited to telemetry, satellite tracking and control. These were performed outside India. Hence, it was the company’s understanding that its income was not subject to tax in India.

However, the Indian tax authorities denied the Hong Kong company’s interpretation of the tax law. According to authorities, since the Hong Kong company had entered into agreements with TV companies that were broadcasting programs to India (and the Indian audience was watching these TV programs), the Hong Kong company had business connections in India. Therefore, part of the Hong Kong company’s income was to be taxed in India.

In the first appeal, the Chief Commissioner of Income Tax ruled that the income of the Hong Kong company was not subject to tax in India because of the business connection, however, such income was to be deemed as royalty and therefore taxed in India.

In the next round of appeal, the Indian Income Tax Appellate Tribunal (“ITAT”) found that the Hong Kong company indeed had certain business connections in India, but since it was not engaged in any activity in India, its income was not taxable in the country. The ITAT, however, expressed its opinion that the income had to be taxed in India as royalty.

However, the Delhi High Court further reversed ITAT’s decision on the royalty. According to the High Court, the Hong Kong company could not be regarded as doing business in India merely because its satellite coverage area extended over India. Further, the High Court also took into account the definition of “royalty” in Explanation 2 to Section 9(1)(vi) of the Indian Income-tax Act 1961 (“ITA 1961”) (as amended prior to the retroactive amendment). The High Court noted that the term “royalty” includes, inter alia, “the transfer of all or any rights in respect of […] process.”

Besides, the High Court stated that the Hong Kong company retained control of and operated the satellites as well as provided services to customers without enabling the customers to use any “process.” The signals transmitted by the TV channels were received or processed by transponders attached to the satellites, but those satellites were operated by the Hong Kong company, not by the companies operating the TV channels.

Further, any “process” performed by the transponders could not be considered as “performed in India” since the satellites that carried the transponders were placed outside India. Moreover, according to the High Court, the TV channels (i. e., the customers of the Hong Kong company) had no involvement in the “processes” occurring in the satellites’ transponders.

Given the above, the High Court found that the Hong Kong company’s income was not royalty taxable in India under Section 9(1)(vi) of ITA 1961.

Following this, in 2012, the definition of “royalty” in Section 9(1)(vi) of ITA 1961 was amended with retroactive effect to overcome the above judgment of the Delhi High Court. As a result of this amendment to the definition of “royalty,” the transmission of signals via satellite is now deemed as “process.”

Thus, under the amended ITA 1961 definition, income of a foreign satellite owner from transmission of signals of a TV channel doing business in India is deemed as “royalty” accruing in India and hence taxable in India.

Notably, the retroactive effect of tax duties in this field has led to escalation of tax disputes as well as immediate cash outflows, which has negatively impacted India as a market for the TV business. Some tax experts believe that the retroactive effect of the amendments to the domestic tax legislation significantly contradicts basic legal principles.

4. Unauthorized Launch of NanoSats

In 2017, US-based Swarm Technologies designed a constellation of small communication SpaceBee satellites and was ready to launch them into orbit. However, the US Federal Communications Commission (FCC) rejected the application to launch these satellites due to safety concerns.

These cubic NanoSats, with faces only 1 inch long, were too small to be tracked from Earth via the US Space Surveillance Network. This system tracks all human-made objects in orbit, which must be at least 4 inches on each side. This size is commonly known as 1U. Satellites smaller than this size pose a large and uncontrollable threat to other spacecraft.

This, however, was not an obstacle for Swarm Technologies. It turned out in January 2018 that despite the revoked launch license, the satellites were launched as a payload on India’s PSLV rocket.

During the subsequent investigation, the main question was whether the satellites had actually been launched. In fact, the evidence of placing SpaceBees into orbit seems indisputable. The PSLV mission documents describing the rocket, its properties, and payload all referred to SpaceBees NanoSats in several passages. Web services tracking satellites also indicated SpaceBees in orbits nearly identical to those specified in Swarm Technologies’ application. Also, the Spaceflight website showed that the company had indeed delivered 19 of the 31 satellites for the PSLV launch in January 2018, including some with SpaceBees’ unique 0.25U size.

Another question was how Swarm Technologies managed to launch its satellites without FCC license. Jenny Barna, launch manager at Spire Global, noted that on the one hand, it is usually necessary to provide a license to the launch operator before the satellite can be installed on the rocket. On the other hand, this is a lengthy process, and in some cases the license was obtained at literally the last moment, when both rocket and satellite were already on the launch pad. “The Silicon Valley way of doing things is technically pretty iterative. […] We’ve had satellites on the launch pad before the FCC approves it, and then they approve it at the last second.” As a result, it is unclear whether Swarm Technologies relied on a last-minute license, as many other space startups do, or whether they negligently or intentionally failed to remove the satellites from the rocket.

The investigation ended with the FCC fining the company $900,000 at the end of 2018. In fact, even the FCC officials admitted that this fine was not sufficient enough, however, the case itself has shocked not only regulatory authorities, but also private space companies, as they had been expecting the severe consequences, such as restrictions on space licensing.

This case was not brought to court, although the company was sanctioned with both penalties and harsh restrictions. Even so, already in 2019 Swarm Technologies managed to meet the regulator’s requirements and obtained a license to launch 150 satellites.

5. Dispute with Canada over Soviet Cosmos-954 Satellite Crash

Perhaps this classic case of public international law is unfairly addressed at the end, but there is always room for dessert.

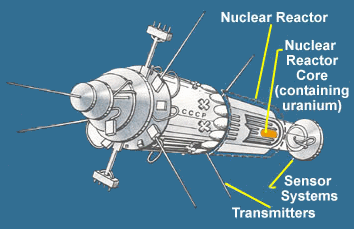

The Soviet Cosmos-954 satellite was launched from the Baikonur launch site on September 18, 1977, which was officially reported to the UN Secretary General. The satellite was paired with the Cosmos-952 twin satellite launched two days earlier.

After 43 days of operation, Cosmos-954 began performing strange maneuvering in orbit, and then communication and control over it were lost. It is believed that the reason for this was the collision with space debris, which caused depressurization of the spacecraft.

It was not possible to move the satellite to a higher orbit and bury it there. On January 6, 1978, the instrument compartment was depressurized, and the spacecraft became a total loss and no longer responded to commands from the control center. The uncontrolled satellite finally entered the Earth's atmosphere, and the USSR officially informed the US of this.

Under the influence of atmospheric drag, the satellite began to rotate rapidly and descend until finally, on January 24, it entered the dense layers of the atmosphere and broke apart, partially burned up, over northwestern Canada.

As a result of the satellite fall, more than a hundred radioactive debris fragments were scattered over an area of about 124,000 kilometers2, i. e., about 10% of Canada’s Northwest Territories. Due to the low population of the area and the large scattering of radioactive debris, the likelihood of people being affected by radiation was low. Rapid absorption of radiation was also due to the high number of rivers and lakes around.

Canadian specialists were searching for the fragments of the “space wanderer” jointly with the Americans and refused the assistance of Soviet experts. As a result of the Operation Morning Light, so named because the satellite fell in the early morning, some parts of the Cosmos-954 were found in the Great Slave Lake and near Uranium City.

The Operation began with an airborne probe of the area using airplanes and helicopters. After the 800-kilometer fall area was determined, the second phase of the Operation started, namely a search for the satellite debris. In total, more than 100 fragments were discovered in the form of rods, disks, tubes, and smaller parts with radiation ranging from a few milliroentgens/hour to 200 roentgens/hour and a total mass of 65 kilograms. All in all, more than 90% of the radioactive fission products from the satellite reactor were collected. The cost of the Operation amounted to $14 million.

The fall of this Soviet spy satellite with a nuclear reactor and the subsequent radioactive contamination of the NATO territory caused a huge international scandal. The USSR government had to officially confirm the fact of launching satellites with nuclear reactors and pay compensation to Canada for the contamination of its territory with the satellite radioactive debris.

According to the document named “Settlement of Claim between Canada and the Union of Soviet Socialist Republics for Damage Caused by “Cosmos 954” released on April 2, 1981, Canada estimated the expenses incurred to liquidate the consequences of the fall at about 6 million Canadian dollars and insisted that the USSR recover additional expenses that might arise in the future.

The USSR argued that Canada had failed to comply with its obligations under Article 5 of the Liability Convention (1972), under which Canada was required to allow the damaging party to participate in the Operation Morning Light in order to minimize the damage caused. Besides, the definition of “damage” in the Convention did not include damage to the environment.

Finally, the USSR compensated Canada with 3 million Canadian dollars for all the circumstances that were caused by the satellite’s fall. The above document was signed in Moscow by Geoffrey Pearson, Canada’s Ambassador to the USSR, and N. Ryzhkov, Soviet Deputy Foreign Minister.

The USSR also had to stand down from launching such satellites for almost three years and seriously improve the satellite's radiation safety system. The USSR also had to stop launching such satellites for almost three years and to significantly improve the radiation safety systems of its satellites.

* * *

This and other articles on space law are prepared by our attorneys from our dedicated Space Law legal practice.

Contacts

.svg)

.svg)

.svg)

New York, NY 10003-1502