Simple Agreement for Future Tokens or SAFT. You have probably encountered it if you have been in the crypto market for at least one cycle. Let’s look into the key terms of these agreements and highlight the main points for negotiations. This checklist provides key information for those outside the legal field but we, of course, strongly advise engaging a lawyer before entering into any binding agreements.

SAFTs may be referred to as token warrant agreements or token side letters, but essentially they serve the same purpose. One party initiates a transaction to issue a certain number of tokens in the future to another party in exchange for payment today.

The original SAFT first appeared in 2017 and was designed to serve as a standard template like its predecessor SAFE from Y Combinator. However, it is important to note that SAFTs do stray from the standard template and can be tailored to provide protection for both the company and the purchaser. There is no industry-wide standard, so don’t be confused if someone is insisting on completing a deal “under the terms of the original SAFT.” We will refer to the original SAFT multiple times in this article for comparison and to provide a historical perspective; however, do not interpret this as an endorsement of its terms.

Key Definitions

The SAFT usually has the following defined terms:

- “Company” – the issuer of tokens

- “Purchaser” – the buyer of tokens

- “Purchase Amount” – the total price to be paid by the Purchaser

- “Network” – a rough description of the protocol or platform to be launched by the Company

- “Network Launch” – definition of when the Network is deemed launched

- “Token” – the name of the token to be issued by the Company, which is usually defined as “a unit of value in the Network”

- “Deadline Date” – the date by which the Network is expected to be launched

- “Termination Events” – a list of events when the SAFT terminates, as well as the Deadline Date

We do not capitalize these terms when we use them in this article.

Deadline Date

Under the original SAFT, the purchaser receives the tokens if the network launches before the termination of the SAFT. The consequences of termination are dependent on the type of termination event and range from a total refund of the purchase amount to its full write-off. We will discuss termination in more detail below.

This aspect of the SAFT was included to protect the purchaser so that the purchaser can receive funds back if the network does not launch. However, as SAFTs evolved during a seller’s market, it has become common to see SAFTs without a specified deadline date. If there is no deadline date to launch the network in the SAFT, the purchaser is effectively providing the company with an interest-free loan for an indefinite term, similar to the SAFE.

For example, in the Telegram token sale, both the “deadline date” and “termination amount” as defined in the transaction documentation allowed investors to recover some funds after the SEC halted the sale in 2018.

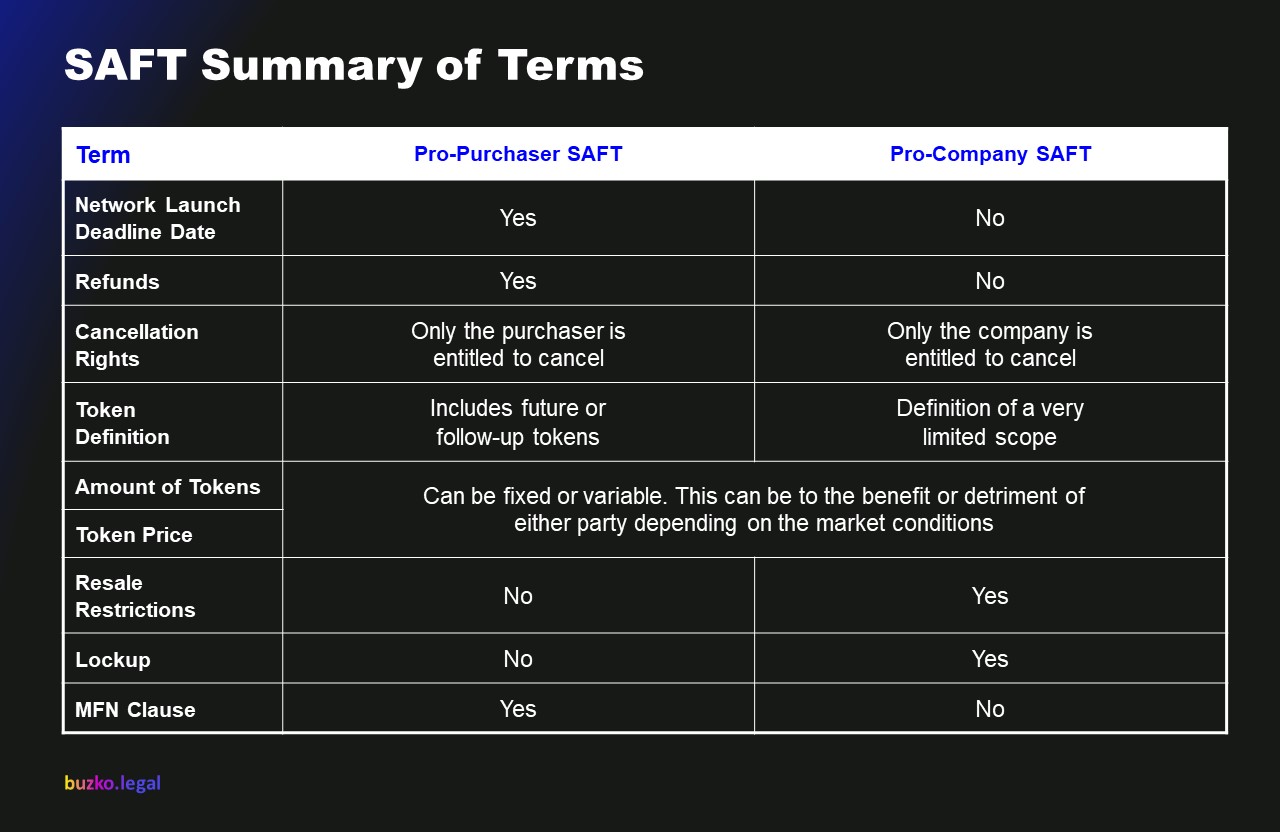

TL;DR: Check whether the SAFT includes a deadline date that is prior to the expected launch of the network as well as the consequences if the network is not launched by that date. Investors prefer time-bounded commitments. Token issuers prefer not to have such a date.

Cancellation Rights

SAFTs vary significantly in terms of cancellation rights. The original SAFT provides for several termination events, including the failure to launch the network by the deadline date and the failure to raise a certain amount of net proceeds from the sale of tokens. It does not grant any cancellation rights to the company.

Purchasers need to be aware that subsequent modifications of SAFTs do not necessarily provide them with such cancellation rights. Moreover, in those SAFTs, the company can have the right to terminate the deal and return the purchase amount to the investor.

Just like with the deadline date, the cancellation provisions are largely influenced by current market dynamics. In a seller’s (token issuer’s) market, investors may be willing to consent to less favorable terms.

TL;DR: Check if there are any cancellation rights granted to either or both parties.

Refunds

There are at least three distinct scenarios when refunds may be due under the SAFT:

- The network does not launch prior to the deadline date;

- There is a dissolution event prior to the termination of the SAFT such as voluntary or involuntary dissolution of the company; or

- One party cancels the SAFT, if it has the right to do so.

The SAFT should regulate the above cases and define the amount to be refunded. It is not uncommon to see that purchasers under SAFTs are entitled to receive back the purchase amount less certain expenses incurred by the company by the refund date.

TL;DR: Check whether there are any refunds under the SAFT and how they are calculated.

Token Definition

SAFTs usually define tokens in a somewhat vague manner such as “a unit of value in the Network.” This exclusion is not due to an oversight of a particular SAFT, but rather because it is hard to give a precise definition without limiting the company in designing the network and its token economics.

For instance, the company may decide to issue several distinct tokens, like in the dual-token structures that have gained popularity recently. As an investor, you want to ensure that you will receive an allocation of any tokens issued by the company in future. As a token issuer, you should keep this in mind when designing the network.

TL;DR: Check the definition of “tokens” to see whether it includes future or follow-up tokens, if any.

Amount of Tokens

The SAFT should contain information about the total supply of tokens and the number of tokens reserved for the purchaser. Here are two SAFT examples that could protect the purchaser in this regard.

- The SAFT defines the total supply of tokens and a specific number of tokens to be issued to the purchaser.

- The SAFT contains the purchase amount and the mechanism to determine the price of one token. The purchaser is entitled to receive the number of tokens equal to the purchase amount divided by the price of a single token.

In the first example, the investor has advance knowledge of the number of tokens that are to be received. The second example provides for a more flexible approach whereby the price will be determined by certain future events such as the token sales price in the next financing round. We discuss variable pricing in the next section.

Regardless of the specific mechanism, it is important to note that the percentage of an investor’s tokens does not usually correspond to the percentage of shares that this investor would otherwise have in the company’s stock. This stems from the fact that the total supply of tokens is usually allocated among a broader set of stakeholders than shares of common stock. Based on the research by Lauren Stephanian and Cooper Turley, the optimal token distribution strategy allocates 35% to the team and investors, i.e. the stakeholders that have equity in the world of traditional startups. Therefore, it would be reasonable for an investor who receives 5% in the company’s equity to receive 5% from the 35% of tokens allocated to shareholders, or 1.75% of the total supply. This is particularly relevant for double financing rounds, where the investor receives both equity and a token allocation. You can read more about modern token sales in our Web3 Startup Legal Guide.

TL;DR: Check the definition of the total token supply and what amount of tokens the purchaser will receive. It can be a fixed amount or a formula.

Fixed vs. Variable Token Price

The price of tokens is not always known in advance. While the team may have some estimates, the crypto market is very difficult to predict.

If the project is raising funds during a bear market, the token price may be set at a low enough valuation to attract investors. In subsequent token sales or a public listing on exchanges, the token price may be multiple times higher due to the cycle change. This means that the project has made its early investors very rich at the expense of allocating more tokens to the project development team. In the alternative scenario, if the team is raising capital during a bull market, its early token investors may overpay if the market falls into a downturn when the token is actually issued.

Both scenarios are suboptimal. For this reason, the parties sometimes agree on a variable token price. For example, the company may offer its investors the right to purchase tokens at a discount during the next pricing event. Such an event could occur during the public sale or could be based on the market price when the token is listed on exchanges.

TL;DR: Consider whether the fixed or variable token price is optimal in the current market conditions.

Resale Restrictions

SAFTs usually have restrictions preventing the purchasers from reselling the tokens or assigning the rights within the underlying SAFT on the secondary market prior to the network launch.

This restriction is usually motivated by the desire to limit access to the company’s tokens on the secondary markets prior to the network launch. This also ensures that the company has greater control and visibility over its token economics. Moreover, such restrictions are sometimes required under the applicable regulations such as Reg D or Reg S in the US.

TL;DR: Check whether the SAFT has any resale restrictions and the period during which such restrictions are applicable.

Lockup and Delivery Schedule

In addition to resale restrictions, it is also common to find lockup periods in SAFTs, i.e. periods during which the purchaser may not sell its tokens to any third parties. The lockup period starts running from either the network launch or public listing on exchanges and usually ranges from 12 to up to 36 months. The lockups are designed to prevent the rapid sale of tokens upon listing.

Depending on the network economics, the SAFT may also allow the investor to stake its tokens during the lockup period and receive token rewards from such staking.

TL;DR: Check whether the SAFT has any lockup provisions and their timeline.

Most Favored Nation Clause

The Most Favored Nation (“MFN”) clause is designed to ensure that the purchaser under the SAFT has no less favorable terms than other investors in the financing round. If the company subsequently enters into SAFTs that are advantageous for the purchaser holding this SAFT, the purchaser may choose to amend the SAFT to reflect the terms of the later-issued SAFTs.

MFN clauses were uncommon in early SAFTs, but are now appearing more often.

TL;DR: Check if the proposed SAFT has MFN provisions and incorporate them if necessary.

Summary

While the original SAFT was drafted with the intent of becoming an industry standard, there is no such standard as of 2022. Whether you represent an investor or a token issuer, having a solid understanding of SAFT terms and protections before you enter into an agreement is key to avoiding legal issues in the future.

Contacts

.svg)

.svg)

.svg)

New York, NY 10003-1502