Once you’ve decided to establish a C-corporation, you immediately have to deal with the issue of distributing shares, even before you file any incorporation papers with the state. The first thing you need to decide is, how many shares will the company have?

To properly answer this question, it’s important to clearly grasp the difference between “authorized” and “issued” shares.

- Authorized shares are shares that the corporation may issue pursuant to its Certificate of Incorporation (COI).

- Issued shares are shares that the corporation has already issued to its shareholders.

IMPORTANT! If you don’t have the time to read the entire article, at least remember this: the number of issued shares may not exceed the number of authorized shares.

Next, we’ll look in greater detail at the nuances of stock distribution and offer some tips on how to formalize such distribution correctly.

Authorized Shares

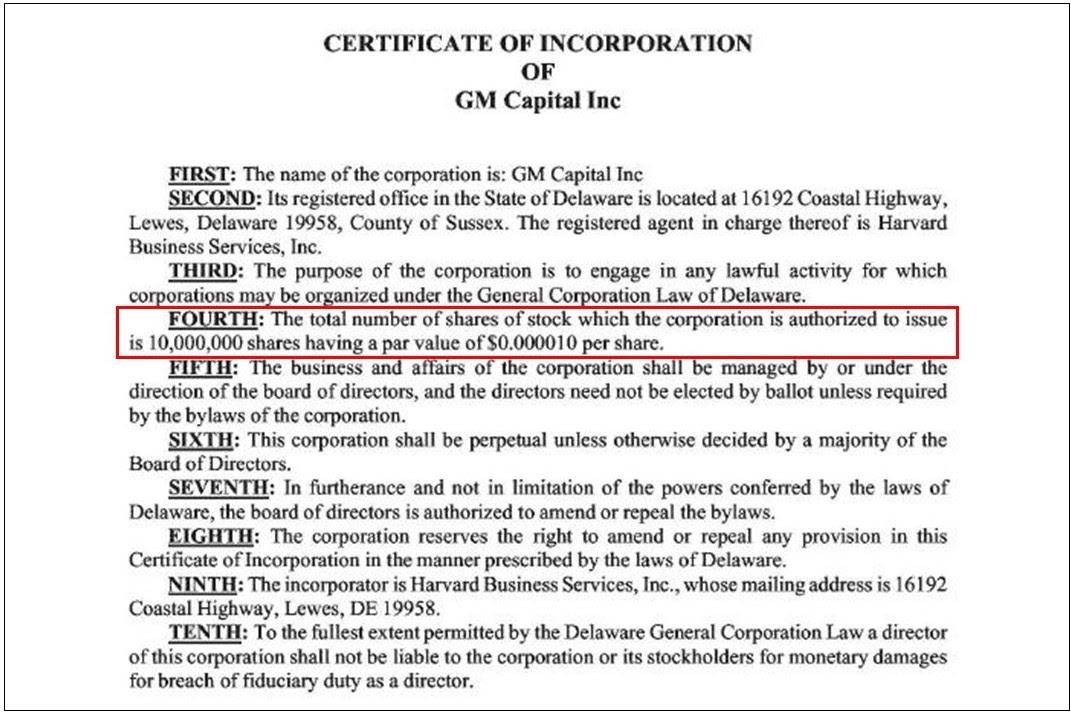

Authorized shares are determined in the COI, which also specifies their type – “common” or “preferred,” as well as their number and par value.

Common shares are shares that the founders divide among themselves. The COI can specify any number of authorized shares, but for startups intending to fundraise and issue options to their employees, the recommended number is 10 million authorized shares of common stock having a par value of $0.00001 per share.

An example of a COI provision authorizing stock can be found below:

Par Value of Shares

The par value per share specified in the COI establishes the minimum share price at which transactions involving the transfer of the company’s shares can be executed. In order to let founders buy shares in their own C-corp cheaply, this threshold is usually set at a level where the total purchase price for all of the company’s shares does not exceed $100. Thus, if we were to use the COI example above, a founder in whose favor the company issues 5 million shares would have to pay $50.

It should be noted that the par value of shares is entirely separate from their market price, so there’s nothing preventing their sale to an investor at a price hundreds of thousands or even millions of times higher than their par value. Just remember that the price at which shares are sold to investors is often used as a benchmark for their fair market value, which, in turn, affects the company’s valuation. Along the same lines, it is considered best practice not to sell common stock to investors, using it only for issuance to founders and employees, and designate classes of preferred stock to investors at each financing round. The idea here is to avoid confusion in the fair market value of common shares so as to prevent founders and employees from incurring an excessive tax burden when they sell their shares. (Note, however, that this view is not shared by everyone – see a differing opinion here).

If you’ve already decided at the incorporation stage that you’ll be fundraising from professional VCs, it would be prudent to include preferred shares in the COI right away. Delaware corporate law makes it possible to do this without specifying all of the rights of preferred stock owners at the incorporation stage by using what’s called “blank check” preferred stock. The corporate rights conferred by these shares are determined during the future investment round.

Issued Shares

Once the company has authorized the type, number, and par value of its shares in the COI, it can distribute them among its initial shareholders. To do this, the corporation needs to authorize the issuance of stock via a resolution of its board of directors and enter into stock purchase agreements with the shareholders (founders or investors).

Remember that the number of issued shares cannot exceed the number of authorized shares specified in the COI. But how many shares should the company issue? Startups traditionally distribute anywhere from 30% to 60% of their authorized common shares among founders. Thus, if a C-corp has authorized 10 million shares, the founders should distribute no more than 3-6 million among themselves.

But why not distribute all of the authorized shares? Because that would prevent you from issuing stock to a new shareholder without having to go through the process of authorizing more shares in the corporation. This is an unfortunate archaic feature of Delaware law, but any stock issuance in excess of the authorized number of shares may be legally void. So to properly increase the number of its authorized shares, the company needs to amend its COI and file it with the Delaware Department of State. While this is not a complicated or overly costly procedure, it may still be an unwelcome hiccup when you’re trying to quickly onboard a new shareholder. So, if you’re just starting out, it’s best to leave around 40% of your authorized stock unissued.

Ownership Stakes

One aspect that founders frequently misunderstand is that authorized shares have no effect whatsoever on the relative ownership stakes in the company, only issued shares do. For example, if a company with 10 million authorized shares has two founders, the first of whom was issued 1 million shares and the second was issued 4 million, their ownership stakes would stand at 20% and 80% respectively (not at 10% and 40%, as many people erroneously believe). This is yet another reason why distributing all authorized shares right away makes little sense.

Authorized but Unissued Shares

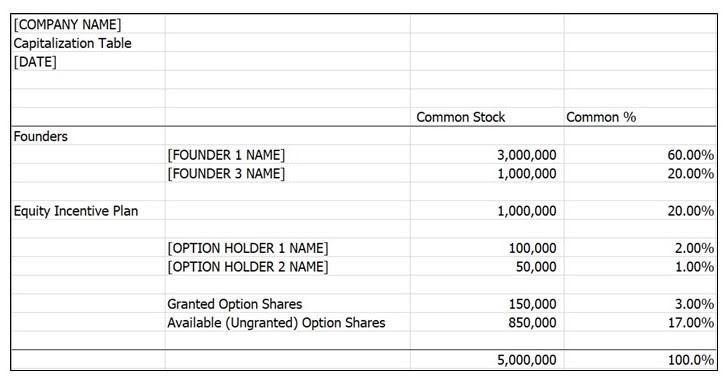

There’s a certain nuance associated with employee equity incentive plans, a.k.a. option pools. Despite the fact that shares reserved for the option pool have not formally been issued, they are counted when determining the shareholders’ ownership percentages. Such shares are referred to as “shares reserved for future issuance.” This is what it looks like in a company’s capitalization table (the Excel file can be downloaded here).

Impact on Franchise Tax

One last point worth mentioning on this topic concerns taxes. The number of both authorized and issued shares has an impact on the amount of Delaware franchise tax a corporation has to pay. For a C-corp whose authorized shares have a par value, the tax is calculated using a rather complicated formula known as the assumed par value method, which you can read about in greater detail on the state’s official website. In practice, the franchise tax for early-stage startups amounts to roughly $500 a year.

Consolidating the Material

The main features of authorized and issued shares are presented in the comparison table below.

.png)

Congratulations! Now you can avoid making mistakes when distributing the shares of your C-corp and show off your newfound knowledge to your startup friends.

Contacts

.svg)

.svg)

.svg)

New York, NY 10003-1502