An explanation of the mechanics and shortcomings of the most popular instrument for investing in startups, plus our solution

In 2013, the leading US accelerator Y Combinator released a new financial instrument designed to simplify and standardize seed-stage investments in startups. It was named to reflect its intended purpose: “Simple Agreement for Future Equity” or “the SAFE.” Since then, the SAFE has conquered the venture capital world in the US and beyond, undergoing numerous modifications and inspiring various similar instruments along the way.

However, there’s one issue: the only “simple” thing about the agreement is its name. While the agreement itself runs just seven pages long, the accompanying official instructions take up a full 31 pages. The complexities associated with the SAFE have been discussed in a raft of articles. The opaqueness of its mechanics have been confirmed in our practice. The typical inquiry goes something like this: “Hi! We have a C-corp in Delaware and we’re fundraising – we’ve decided to go with the SAFE. Can you explain how it works?”

Sure we can, and we do, but it’s still mind-boggling how people could settle on a financing instrument without understanding how it works. The SAFE seems to have become a fashionable trend followed by startups and investors alike without a good grip on the details. Still, the SAFE has stood the test of time and appears to be here to stay. That’s why we’ve decided to draft this guide to help the venture capital community better understand the SAFE and to assist you in making an informed choice if you decide to use this instrument for your financing round.

Context: SAFE vs. Other Financing Instruments

To understand the pros and cons of the SAFE, you need to have at least a basic grasp of the other most common startup financing instruments. Here is a brief explanation of the other two most popular instruments along with the SAFE:

- Equity: the investor invests a certain amount of money in exchange for a particular number of shares in the company.

- Convertible note: the investor lends a certain amount of money to the company and, at the end of the loan term, the company either repays the loan plus interest or converts the total amount into shares.

- SAFE: the investor invests a certain amount of money in the company in exchange for the right to receive the company’s shares in the future under certain conditions.

The SAFE was invented to address well-known problems associated with the first two instruments.

What’s Wrong with Selling Shares?

In order to sell equity, the company needs to have a certain valuation to arrive at a defined per-share price. This isn’t a problem if the company has already been in business for several years and has a track record of sales or at least a product prototype. But it’s virtually impossible to assign a fair valuation at the initial (where there is only an idea) or market-testing stage, which is precisely when the seed round of investments mainly occurs. The SAFE makes it possible to invest without assigning a valuation to the company at the time of investment.

An equity sale also entails hammering out the terms of the shareholders’ agreement or the rights of holders of preferred stock, which often requires getting attorneys involved. The SAFE makes it possible to delay these activities until a more experienced investor arrives on the scene.

What’s Wrong with a Convertible Note?

Much like the SAFE, a convertible note allows you to put off the company’s valuation and to agree on the rights of holders of preferred stock until a later date; however, it is a bit more complicated than that. Unlike equity, a convertible note results in the company being in debt to the investor. If the amount of this debt has not been converted into the company’s shares within the note’s term, it must be repaid to the investor together with any accrued interest.

For most early-stage startups, the prospect of making such repayment is grim insofar as, according to statistics, the majority of startups go out of business and therefore would lack the funds needed for repayment. Even promising companies would have their financial condition significantly undermined by a high volume of debt. The SAFE, on the other hand, works like a convertible loan, but is not considered debt because it doesn’t have to be repaid by a certain date.

This makes it obvious why startups have almost universally embraced the SAFE. But the instrument’s popularity among investors also reveals an understanding among them that most of the early-stage investments they make will never be repaid, so they might as well treat those investments like a gamble rather than a loan they might someday get back.

The SAFE Solution

So, to recap, investors like the SAFE because it allows them to invest in a startup without having to assign it a valuation, and startups like it because they get to use outside funds to grow without having to give away equity or become saddled with debt. Sounds great, but the SAFE has its own set of shortcomings. To really understand them, however, you first have to get to the bottom of how the SAFE actually works, so this is what we’ll tackle next. We’ll dispel just one common misconception right away: the SAFE doesn’t make the investor a company’s shareholder. Prior to the SAFE’s conversion into equity, the investor has no rights in the company whatsoever.

How the SAFE Works

Key Terms

To understand how the SAFE works, you first have to understand its key terms.

- Purchase Amount: amount of the investment to be provided under the SAFE.

- Valuation Cap: the highest valuation of the company at which the investor can receive the company’s shares upon conversion.

- Discount Rate: amount of discount that the investor receives to the per-share price upon conversion.

- Equity Financing: investment round during which the company raises funds through the sale of preferred shares to investors. This is the event that triggers the SAFE’s conversion into the company’s equity.

- Liquidity Event: the sale of the company to another company or the company’s initial public offering.

- Dissolution Event: winding up or liquidation of the company.

Y Combinator offers several versions of the SAFE, and the agreement has undergone significant changes since its first appearance in 2013. In this article, we examine the current version of the SAFE, the Post-Money SAFE Version 1.1.

What the SAFE Offers the Investor

Whatever version of the SAFE you are using, it has these common features:

- Upon the occurrence of an Equity Financing, the investor receives shares of the company’s preferred stock.

- Upon the occurrence of a Liquidity Event, the investor receives a payout equal to his proportional share in the company’s capitalization immediately prior to the Liquidity Event.

- Upon the occurrence of a Dissolution Event, the investor receives his Purchase Amount back or, if the company has insufficient funds for full repayment, his proportional share of the company’s available assets.

Even with different versions, the only thing that changes under the SAFE is the stake in the company that the investor receives upon the occurrence of an Equity Financing or the amount of money he receives upon the occurrence of a Liquidity Event.

Next, we’ll look in greater detail at the mechanics of the following versions of the SAFE: (1) Valuation Cap only, (2) Discount Rate only, and (3) both. In all of our examples, we’ll use scenarios with the following fixed inputs:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Discount Rate: 80%

Variables:

- SAFE version

- Company valuation at the Equity Financing (Post-Money Valuation)

Post-Money SAFE – Valuation Cap Only

We’ll start with the version that includes only the company’s post-money valuation cap. “Post-money” means that the company’s valuation includes the amount of the pending investment. For context, there’s also a term known as “pre-money valuation” – the company’s valuation prior to investment. Here’s a simple example:

- Company’s valuation before the investment (Pre-Money Valuation): $900,000

- Investment amount (Purchase Amount): $100,000

- Company’s valuation after the investment (Post-Money Valuation): $1,000,000

The current version of the SAFE uses post-money valuation, so the post-money valuation specified in the agreement is inclusive of the Purchase Amount.

Scenario 1

The inputs under the first scenario are as follows:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Post-Money Valuation: $4,000,000

Note the last figure above – it indicates that after entering into the SAFE, the company has raised a new round of financing at a post-money valuation of $4,000,000. The stake that the investor stands to receive under the SAFE as a result of the conversion is determined as follows:

- $100,000 / $4,000,000 = 2.5%

We’re using the $4,000,000 figure because it’s below the company’s valuation cap ($5,000,000), making it more favorable to the investor.

Scenario 2

Let’s change the inputs as follows:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Post-Money Valuation: $6,000,000

In this instance, the company’s valuation during this round ($6,000,000) is above the valuation cap of $5,000,000, so we use the following threshold to calculate the investor’s stake under the SAFE resulting from the conversion:

- $100,000 / $5,000,000 = 2%

Post-Money SAFE – Discount Only

In this version, the stake that the investor receives upon conversion is always tied to the company’s valuation during the Equity Financing round, but the investor gets a discount on that valuation in the amount specified in the SAFE.

- Purchase Amount: $100,000

- Post-Money Valuation: $6,000,000

- Discount Rate: 80%

Let’s calculate the investor’s stake at the time of conversion:

- $100,000 / ($6,000,000 x 80%) = $100,000 / $4,800,000 = 2%

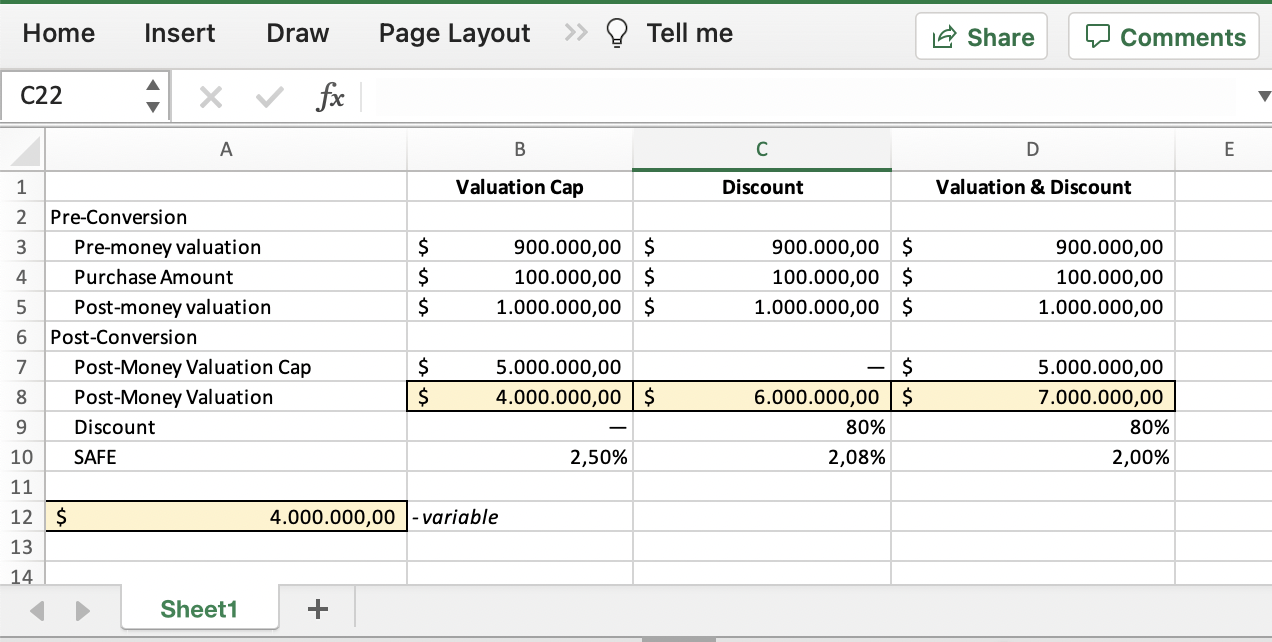

Post-Money SAFE – Valuation Cap and Discount

This version uses both the valuation cap and discount, and the SAFE is converted at the lowest price for the investor.

Scenario 1

The inputs under the first scenario are as follows:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Discount Rate: 80%

- Post-Money Valuation: $4,000,000

Here, the company’s valuation during this round is below the valuation cap, making conversion using the discount the most favorable option for the investor:

- $100,000 / ($4,000,000 x 80%) = $100,000 / $3,200,000 = 3%

Scenario 2

Let’s change the inputs as follows:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Discount Rate: 80%

- Post-Money Valuation: $6,000,000

Next, let’s calculate which conversion terms would be the most favorable for the investor. First, we take conversion using the valuation cap:

- $100,000 / $5,000,000 = 2%

We compare this with conversion using the discount:

$100,000 / ($6,000,000 x 80%) = $100,000 / $4,800,000 = 2%

There’s no difference – the investor gets 2% either way.

Scenario 3

Let’s change the inputs again:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Discount Rate: 80%

- Post-Money Valuation: $7,000,000

Once again, we compare the conversion terms, starting with the conversion at the valuation cap:

- $100,000 / $5,000,000 = 2%

We compare this figure against the conversion at the discount:

- $100,000 / ($7,000,000 x 80%) = $100,000 / $5,600,000 = 1.8%

Here, the most favorable option is conversion at the valuation cap, so that’s what will determine the number of shares the investor will get.

You can model all of these scenarios with different values using the table accompanying our version of the SAFE (you can download both templates here).

Right to Proportional Participation (Pro Rata Right)

In the original version of the SAFE, investors also gained the right to participate in subsequent financing rounds on a proportional basis (pro rata right). At a certain point, however, the agreement’s creators decided that this term was too friendly to investors, so the basic SAFE template no longer includes it. For those who still want a pro rata right, the Y Combinator offers a boilerplate Pro Rata Side Letter, which the parties can execute along with the SAFE.

The Pro Rata Side Letter entitles the investor to participate in the next Equity Financing round within the scope of his proportional stake, which is determined as the ratio of (x) the number of shares that the investor receives from the conversion of the SAFE with a Post-Money Valuation Cap to (y) the company’s capitalization.

Let’s look at an example using the previous inputs. The investor has entered into a SAFE with the following terms:

- Purchase Amount: $100,000

- Post-Money Valuation Cap: $5,000,000

- Post-Money Valuation: $6,000,000

The valuation cap is used at the time of conversion, and the investor receives the following stake:

- $100,000 / $5,000,000 = 2%

Consequently, by leveraging his pro rata right, the investor can acquire up to another 2% of the shares issued during the financing round to maintain the ownership stake that he receives as a result of the SAFE’s conversion. Thus, if the investor were to exercise his pro rata right in full, he would own 2% of the company’s shares after the Equity Financing. Conversely, SAFE investors who either don’t receive or don’t use their pro rata right are diluted by the shares issued in the Equity Financing.

The SAFE’s Shortcomings

As we’ve already mentioned, the SAFE is very attractive to startups since it allows them to raise and use investor funds without immediately offering anything in exchange. But the standard SAFE template from Y Combinator also has significant shortcomings. We will examine them below in descending order of negative impact.

1. The SAFE Doesn’t Contain a Minimum Equity Financing Amount for Triggering the Conversion

Let’s start with the definition of Equity Financing in the SAFE template (Section 2):

At first glance, this might only seem to be a problem for the investor, as no one wants to be a shareholder in a company that has raised a small round and is not showing promising results. But such a situation might also be undesirable for the company: for example, if the company issues preferred stock at a small round to raise the funds necessary for its further development, it might be disadvantaged by suddenly gaining a bunch of new shareholders from the automatic conversion of the SAFEs.

The solution to this problem might be establishing the minimum amount of a round triggering a conversion. For example, for many companies, $200,000 raised is a rather serious signal that development is going in the right direction and that the company is ready to move to the next level with its new shareholders.

2. The SAFE Has No Maturity Date

The SAFE terminates upon the occurrence of an Equity Financing, Liquidity Event, or Dissolution Event. But what happens if none of these events occur within a reasonable amount of time?

In this respect, the SAFE is once again inferior to traditional convertible loans that have a maturity date by which the loan must either be converted into shares or repaid to the investor. It’s not uncommon for companies that have started off by raising venture capital to successfully develop on their own without additional raises from investors. But if such a company has raised its initial round using the SAFE, its investors are unlikely to become shareholders, but their theoretical right to do so can be a persistent distraction for the company.

Such a situation could easily be avoided by establishing a reasonable maturity date in the SAFE. For instance, if conversion does not occur within three years of investment under the SAFE, the company would simply repay the funds to the investor: the investor would be happy to receive his money back, and the company would be relieved to rid itself of potential claimants in the future.

3. The SAFE Contains a Representation that the Investor Is Accredited

Pursuant to Regulation D of the U.S. Securities Act, a company raising funds via SAFE must obtain a representation regarding the investor’s accredited status (Section 4(b)):

Put briefly, a private individual acting as an investor is accredited if he:

- has a net worth, whether individually or jointly with a spouse, of at least $1,000,000; or

- has had (i) income in excess of $200,000 over each of the past two years or (ii) a joint income in conjunction with a spouse in excess of $300,000 over the same period.

Many investors from non-US jurisdictions investing in startups using the SAFE don’t satisfy these requirements. Consequently, they’re breaching the terms of the SAFE, putting their future rights to the company’s shares at risk, while the company is violating US law by failing to take reasonable measures to ensure that the investor is actually accredited.

This problem can be solved by swapping the accredited investor representation under Regulation D for a representation that the investor is not a US resident and will refrain from selling his SAFE to any US residents. This representation would allow for the investment to be governed by Regulation S, which covers the sale of securities to US non-residents, who are not required to be accredited investors.

Our solution

We’ve spent a great number of hours developing a SAFE template that eliminates these and other deficiencies in the YC template. In our version, all variables are spelled out on the first page to avoid omitting important terms, and the agreement itself is drafted in plain English that non-lawyers can understand.

.svg)

.svg)

.svg)

.svg)

.svg)