This article focuses on the main trends in structuring venture funds, including Rolling Funds, Cell-Funds, and RIAs.

The market for investment vehicles is constantly developing, and a venture capital fund isn’t a single type of fund but rather an umbrella name for a group of funds, some of which we discuss in this article.

We are often approached by clients who want to set up a venture capital fund but don’t know all the options. Different structures may be optimal for different purposes. More details about our services can be found on our website.

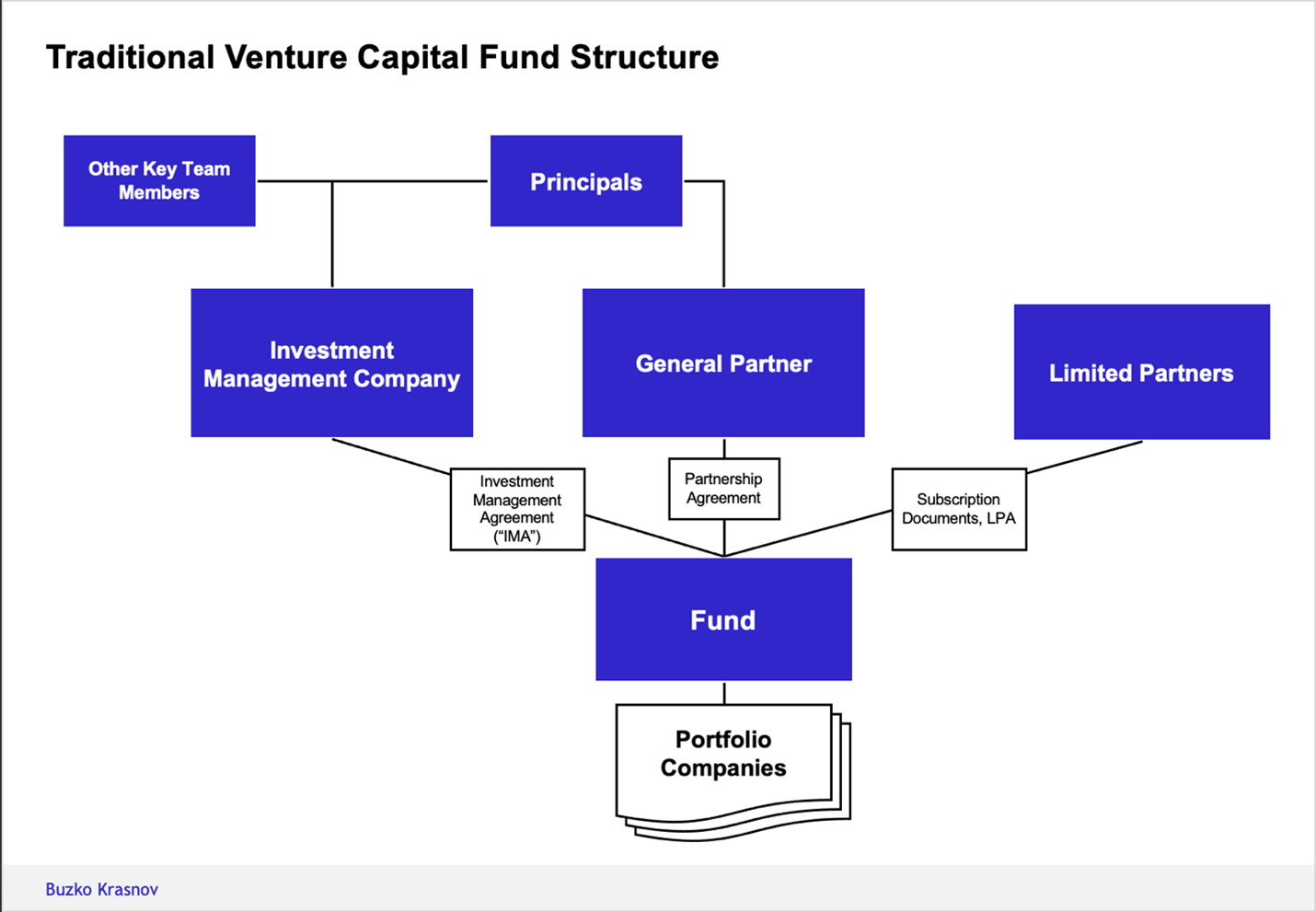

Traditional Venture Capital Fund Structure

Historically, venture funds are structured as follows. The fund itself is usually a Limited Partnership (Partnership), managed by a General Partner (GP). The Partnership structure assumes that the GP has unlimited liability (i.e. risks all its property) while the Limited Partners’ liability is limited to their contributions. To minimize risks, the GP is usually formed as a Limited Liability Company (LLC). Thus, the liability of the founders of the GP is limited to their contributions. Investors enter the fund as Limited Partners.

The last entity in the traditional VC fund structure is the Investment Manager (IM) aka Investment Adviser that makes investment decisions. Typically, it’s also an LLC. Sometimes, in “young” funds, the functions of the GP and IM are performed by the same legal entity.

In larger funds, these functions are always separated. For example, if a team manages several funds (with different or successively-created strategies), then all such funds will have the same IM with the same shareholder structure, but different GPs with different teams, the composition of which depends on the required competencies. There are also certain tax reasons for separating these functions.

After the creation of a classic venture fund, its activities depend on the terms of the Limited Partnership Agreement (LPA). Generally, the fund is created for a period of 8 to 13 years, where the first 4-5 years is the period for investing in new companies and the rest is for reinvesting and exiting previous investments. During the life of the fund, investors are limited in their ability to exit the fund.

For a venture fund, the fundraising looks like this: to become limited partners, investors pay a Capital Contribution, usually in the amount of 20% of the total contribution, and the rest upon request by the GP (Capital Calls).

You can download a typical VC fund term sheet on our website.

Rolling Funds

Unlike the classic structure, a Rolling Fund (RF) provides more flexibility in financing. Thus, an investor or LP must regularly (quarterly, for example) contribute a certain small amount, receiving a profit from the part of the portfolio in which the LP has invested. Moreover, an RF investor can increase the amount of its investment at any time, as the amount is not limited by the initial agreements.

For the fund manager, such a structure has both pros and cons. On the one hand, the reduced initial contribution amount and shorter commitment period makes it easier to attract new investors and allows the manager to control cashflow. When a big deal appears on the horizon, the fund manager will call upon existing and new investors to raise capital. On the other hand, when there are no good deals in the pipeline, the RF’s manager may simply pause its activities. This is different from a venture fund, where investors immediately deposit a large amount and even more in the process, and the manager is under pressure to invest the funds somewhere.

But the manager of an RF must also constantly search for investors, and there is no guarantee that, when a huge deal comes up, he will be able to bring enough money to the table. Hence, a traditional venture fund provides more certainty, since during the entire commitment period there is an opportunity to make another Capital Call and request additional funds from investors under the original agreement.

The concept of Rolling Funds was developed by the well-known platform Angellist. There are currently about 80 such funds listed on Angellist, with a minimum investment ranging from $5,000 to $50,000 per quarter.

Series LLC “Funds” Gaining in Popularity

Series LLCs have become increasingly popular in the investment world as of late. We intentionally use the term “fund” in quotation marks, because in essence it is not really a fund.

In a nutshell, the structure of a Series LLC is as follows: a Series LLC consists of a main cell (master LLC) and subsidiary cells (series). These sub-cells are created for a specific transaction or a specific investor. Each such cell is an independent legal entity with separate property and limited liability. This structure makes it possible to isolate the investments of each series from one another and from the master LLC, thereby limiting the risks. This contrasts with a traditional VC fund, where a few bad investments can nullify the profitability of the rest. With series, however, investors in profitable series will not incur losses from unprofitable ones.

Usually, the Series LLC structure is used to provide each investor with the right to choose which deals or projects he wants to enter. In this case, the manager of such a “fund” actually ensures the deal flow but isn’t responsible for the choice and success of a particular investment, because each investor independently decides where to invest.

This is the main difference from a venture fund, where investors’ contributions are pooled, and the success of the entire enterprise depends on the quality of the investment decisions made by the IM.

This, in turn, may lead to a reasonable question about the size of the success fee (carry) for the Series LLC manager. Given that, in a classic venture fund, carry is usually around 20%, what fee would be appropriate for a Series LLC, where the manager is actually only engaged in the search and selection of transactions, but is in no way responsible for the success of the investment?

Venture Fund Advisers Becoming Registered Investment Advisers (RIAs)

Generally, VC fund managers operate in the US as Exempt Reporting Advisers using the Venture Capital Fund Exemption from SEC registration. Under this exemption, an investment adviser may avoid registration with the SEC and only file an annual report for the adviser and his funds if he exclusively advises VC funds.

One of the requirements for a venture fund to qualify under the exemption is a limit of 20% Non-Qualified Investments in the total portfolio. Qualifying assets include securities purchased directly from the company or through one of the national exchanges. For the purposes of the exemption, money, bank deposits, and investments in index funds are not taken into account.

In practice, this limits the share of high-risk assets in a venture fund’s portfolio. This limit also applies to cryptocurrencies and the purchase of shares from founders or early investors.

These restrictions have prompted a number of large venture capital funds, such as Andreessen Horowitz and Foundry Group, to register as Registered Investment Advisers (RIAs). This solution makes it possible to avoid limits on investments in various instruments and assets.

However, there are also certain strings attached. In addition to the higher cost of registration, RIA status introduces significant reporting and compliance obligations, the requirement to monitor all transactions (including those of employees’ relatives), and much more. Therefore, a venture fund that wants to register as an RIA should weigh the benefits against the costs.

In general, obtaining RIA status only makes sense for established IMs with a wide range of instruments in their funds’ portfolios and the means to shoulder the increased regulatory burden. The funds industry continues to communicate with the SEC about easing restrictions on transactions by venture capital funds.

Hedge Funds Make VC Investments through Side Pockets

Typically, hedge funds differ from venture funds in that they invest in more liquid and (presumably) less risky assets, such as shares and derivatives (futures, options, etc.) listed on the stock exchange. Hedge funds generally steer clear of investing in startups because the liquidity of such investments is very low, and hedge fund investors must be able to redeem their shares at any time and claim their investment back. This liquidity gap between a hedge fund’s liabilities and assets leaves investing in startups out of reach for hedge funds.

At the same time, the high return on investments in startups, especially late-stage startups, has been impossible for hedge funds to ignore. This has led to the evolution of the organizational structure of hedge funds and the emergence of so-called side pockets. They work as follows.

A separate side pocket is created in the hedge fund structure, which separates hard-to-valuate illiquid assets from liquid ones. For example, a hedge fund might invest in an early-stage startup whose shares are separated from the general portfolio. The side pocket is usually created as a separate account that investors receive interest on. That said, investors can only receive interest by selling the asset in the side pocket or by transferring it to the main fund. Usually, such a side pocket is not a separate legal entity or a separate class of shares/interests, but simply a mechanism for establishing a separate unique liquidity regime for a part of the investor’s contribution.

As a result, the hedge fund manager can invest in high-risk, low-liquidity investments without fear of a liquidity shortage when the investors decide to redeem their shares.

This structure is gaining in popularity. For example, Tiger Global, which started out as a hedge fund, has now become an active player in the venture capital market. Whereas Tiger Global used to mainly invest in projects at the pre-IPO stage, it recently announced that it would start investing more in deals at earlier stages – up to Series A.

Conclusion

The trends described above demonstrate the market’s desire for more flexible structures. Rolling Funds are designed to both democratize venture capital investment for investors and simplify the launch of funds for managers. Using a Series LLC gives investors a say in choosing trades. The conversion of VCs into RIAs and active investment of hedge funds in startups indicate the convergence of models that have traditionally been viewed as distinct.

.svg)

.svg)

.svg)

.svg)

.svg)