If you’re planning to start a business in the US, you will most likely need to form a legal entity. Currently, the most common company structures in the US are a limited liability company (LLC) and C-corporation (C-corp). In this guide, we will briefly examine the key differences between the two and provide recommendations that will help you choose the most suitable legal entity for your needs.

Before we get into the details, let’s settle on some terminology. Below is a table showing the differences in the terms for the main concepts related to LLCs and C-corps.

Investments

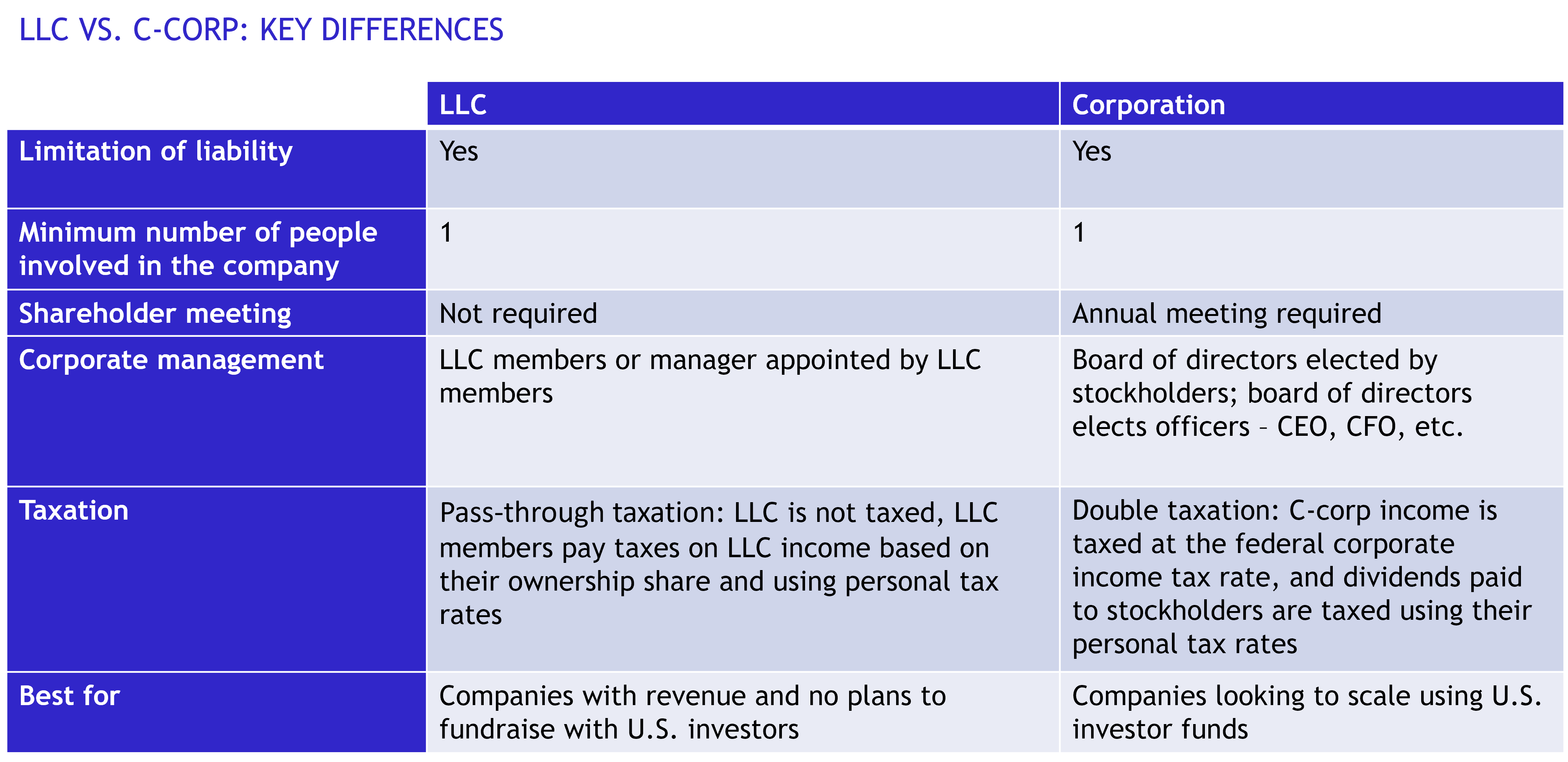

When deciding which entity type is right for you, the main question is whether your company will be attracting investments from angel investors or venture capital funds. If the answer is yes, you will most likely need to form a C-corp.

There are a couple of reasons for that. First, LLCs are less suited for investment purposes from a tax perspective, as we discuss in more detail later in this article. Second, LLCs are quite flexible in terms of company management. This means that, in their articles of organization, LLC members can include just about any limitations of fiduciary duties, restrictions on third-party management of the company, and other modifications of standard provisions. In most cases, such conditions tend to fend off business angels and accelerators because they don’t want to spend huge amounts of time “deep diving” into every nook and cranny of company documents. By contrast, a C-corp is a much less flexible corporate structure, which makes it more attractive and predictable for investors.

Corporate Management

Another advantage of LLCs is that they impose a lower administrative burden on their owners compared to C-corps. One example is that the law does not mandate LLCs to hold annual meetings of their members, so there is no need for an LLC to bear costs related to providing an annual meeting notice, drafting the agenda, holding the meeting, voting on the composition of the board of directors, producing accurate meeting minutes, and sending them to the stockholders – all of which are required for a C-corp.

LLCs can also freely choose how they’re managed: the members may either manage the company directly or hire managers to do so. C-corps, on the other hand, must be managed by their directors, who, in turn, must be elected by the stockholders. The directors may then appoint company officers, such as a CEO, CFO, Secretary, and the like.

Corporate Taxation

An LLC is subject to pass-through taxation, which means that the company itself is not taxable, whereas its members pay business income tax based on their individual tax rates. Therefore, if an investor acquires an interest in an LLC, he may have to bear an additional tax burden if the LLC turns a profit even if the investor has not received any dividends from the company. This is because an LLC’s income is deemed to be earned by its members in proportion to their interests in the LLC regardless of whether this income is actually distributed among the members.

A C-corp’s income is subject to double taxation because, unlike an LLC, a C-corp is a separate entity for taxation purposes and is required to pay income tax. If the C-corp declares and pays any dividends to its stockholders, they are then subject to personal income tax at the dividend recipients’ individual tax rate. On the one hand, this means that, in monetary terms, a C-corp is almost always a less favorable choice when it comes to taxes than an LLC. But, on the other hand, if the goal is to attract investment, then a C-corp’s investors do not have to worry about paying taxes on the company's retained earnings, as is the case with an LLC.

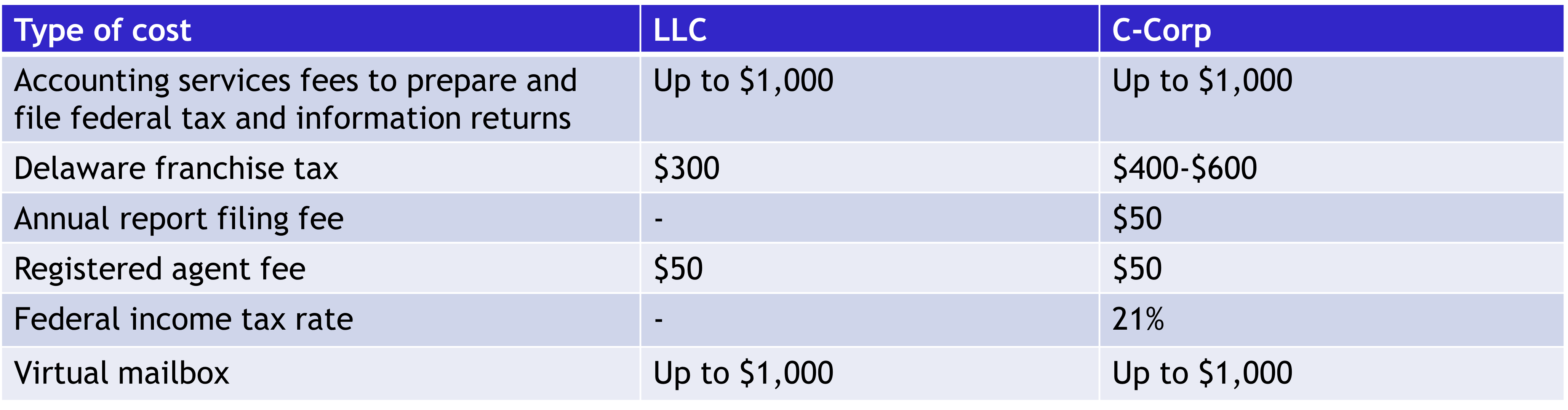

Company Maintenance Costs

The table below shows the main annual maintenance costs for a Delaware LLC and C-corp.

Franchise Tax

The franchise tax is the fee charged by the State of Delaware for the right to keep a company incorporated there. Although the name of the tax can be somewhat misleading, it has nothing to do with a franchise in the traditional sense. Rather, all legal entities formed in Delaware must pay the franchise tax every year to remain in good standing.

The penalty for not paying the franchise tax on time is $200, plus 1.5% of the tax amount owed per every month of delinquency. Failure to timely pay the franchise tax will also prevent you from obtaining a certificate of good standing, which verifies that a company is duly registered with the state, does not have outstanding state registration fees or other required document filings, and is legally permitted to conduct business in the state. The certificate of good standing is often required by banks and other service providers.

LLC Pros and C-corp Cons

An LLC has a number of key advantages over a C-corp:

- Pass-through taxation. An LLC is not taxed as an entity, so its business income is taxed only once using its members’ individual tax rates, which makes it more tax-efficient than a C-corp.

- Transfer of losses. If an LLC operates at a loss, the losses are passed through to the members to be reported on their personal tax returns, thereby reducing the members’ personal tax burden. A C-corp’s losses cannot be passed through to its stockholders.

- Management formalities. LLC management processes are less formalized than those of a C-corp. An LLC is managed by its members or a manager appointed by the members. This makes the LLC more suitable for founders who want to launch operations quickly. Also, unlike a C-corp, an LLC does not require annual meetings of stockholders, which makes its operations more flexible and reduces administrative costs.

C-corp Pros and LLC Cons

A C-corp outperforms an LLC in the following respects:

- Ability to attract venture capital investment and retain profits. Company profits are not automatically imputed to the stockholders, and dividends are taxed only when they are paid to stockholders. A C-corp is thus more suitable for investors, as it allows for keeping their tax burden predictable. LLC members are taxed according to their imputed share of an LLC’s income regardless of whether the LLC’s profits are distributed, making an LLC unsuitable for venture capital investments.

- Employee stock option plans. Founders of C-corps can grant their employees options to purchase company stock in the future at a predetermined price. Employee stock options help founders keep and attract skilled employees and align the interests of the employees with those of the shareholders. LLCs do not have employee stock option plans, although similar types of employee incentive programs for LLC membership interests are becoming more popular.

LLC or C-corp: Which Should You Choose?

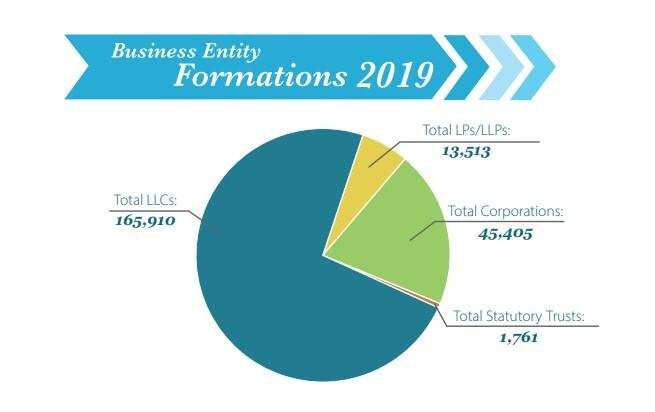

There is no definitive answer to this question, as it depends on the objectives you have set for your business. But there’s a simple rule of thumb: an LLC is a better option for companies that are generating revenue and don’t plan on fundraising with U.S. investors. Statistics show that this is the case most of the time: in 2019, over 70% of all companies registered in Delaware were LLCs.

A C-corp, however, remains the best option for companies planning to participate in acceleration programs and scale through fundraising.

If you are planning to form an LLC or C-corp in the U.S., our U.S. Startup Package provides a turnkey solution to launching your business in the United States.

Contacts

.svg)

.svg)

.svg)

New York, NY 10003-1502