We are glad to present you this brief guide with 10 fundamental tax concepts relevant to digital nomads. The guide will be helpful to online creators, remote professionals, crypto traders, internet entrepreneurs, and pretty much anyone with a location-independent mindset.

Download the cool PDF version here >>

In this guide, we unpack the most important tax issues that digital nomads usually face when planning their business affairs. We’ve aimed to make the guide as broad as possible without focusing on any specific jurisdiction. This approach sometimes comes with the price of omitting desired granularity, for which we take full responsibility. However, we are certain that understanding these general concepts will save you hours and help you speak a common language with your tax adviser.

1. Personal Tax Residence

Personal tax residence is a fundamental concept for digital nomads. Let’s unpack it.

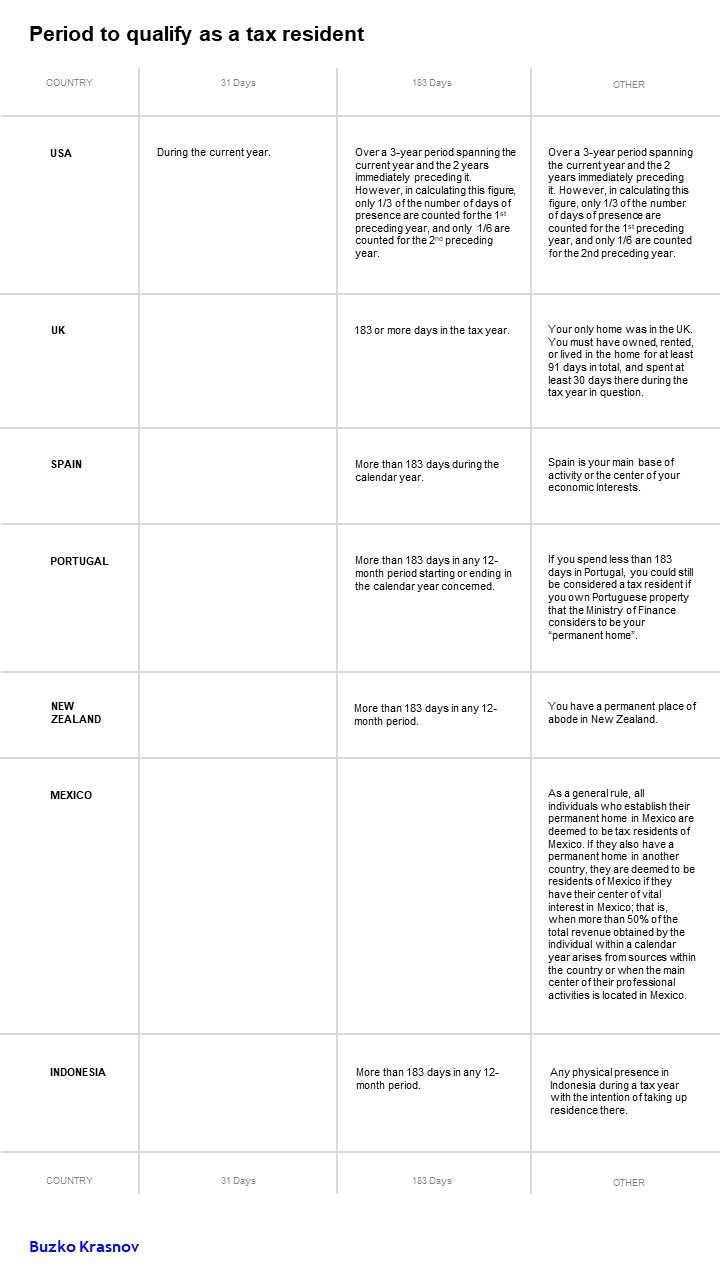

For individuals, the main criterion for determining tax residency is a physical presence. If you are present in a specific country for long enough, you will become its tax resident and will have to pay taxes there. Usually, you must stay in a country for at least 183 days within a 12-month period to be considered a tax resident of that country.

It is generally the case that if you move out of a country, you will stop being a tax resident of that country. However, there are certain exceptions.

Apart from physical presence, some countries apply other tests, such as citizenship and domicile. Citizenship is self-explanatory, but is rarely used as a criterion: the US and Eritrea are the only two countries that tax their citizens regardless of where they live and for how long.

Domicile is a bit trickier. Unlike physical presence, it is a much more flexible concept that relies on factors such as the location of an individual’s main residence and the location of their spouse and children, source of income, and center of economic interests. Domicile usually applies when the physical presence test doesn’t provide clear guidance, such as in the case of tax orphans (more on that below).

To summarize, there are three main criteria for determining tax residence. In descending order of prevalence, they are physical presence, domicile, and citizenship.

Importantly, your tax residence determines not only your tax rate but also which other tax rules you must comply with. For example, if you become a tax resident of the US, then apart from paying US taxes, you also become subject to US rules on controlled foreign companies (more on that below).

2. Tax Orphans

Is it possible to become a tax orphan by constantly traveling and avoiding ties with any single jurisdiction?

Hypothetically, yes. After all, anybody could shrug off tax residency if they were willing to, say, live out their life on an isolated platform in the middle of the sea or relocate to a rocky outcropping high in the Himalayas.

But to shift a little closer to reality, you can qualify as a tax orphan if:

- Your home country exclusively applies the physical presence test to determine tax residency, and has no concept of domicile or “center of vital interests”; and

- You move out of your home country for long enough to lose tax residency; and

- You don’t become a tax resident in any other country by either (i) overstaying a given time period or (ii) having some other ties with that other country under its local law; and

- There is no international arrangement, such as a double taxation treaty (“DTT” — more on that to come), between the countries that you visit which forces you to become a tax resident of one of those countries.

3. Source of Income

States will tax you differently depending on the source of your income. Let’s review this important concept before we go any further, as it is key to understanding both personal and corporate taxation.

The possible types of income are myriad: salary, interest payments, royalties, dividends, and payment from online gigs, just to name a few.

Each country’s tax code makes an initial sorting of these income types by relegating them to one of two general categories:

- Local income, i.e. income generated from sources within the country; and

- Foreign-source income, i.e. income generated from sources outside the country.

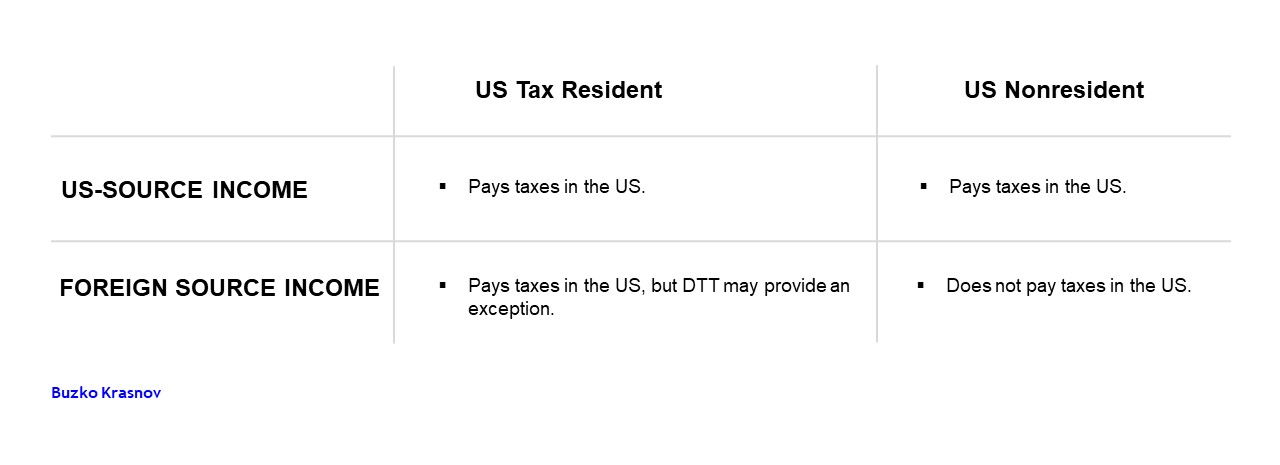

The general rule is that if you are a tax resident of a particular country, you have to pay taxes in that country on both your local and your foreign-source income. Meanwhile, your foreign-source income may also be subject to taxation in the country where it is sourced. To avoid double taxation, you have to rely on a DTT between the two countries.

To illustrate, let’s consider an example. Suppose Frank is a tax resident of the US. He is employed by a US company and receives a monthly paycheck. Frank also owns a condo in Paris that he leases on Airbnb and receives rent payments from. In this case, Frank will owe taxes to Uncle Sam from both his income streams—both his local US salary and his foreign-source French rental income. Furthermore, France will also want a piece of the pie, and will levy their own taxes on his rental income, since it is sourced locally in France.

Seems a bit unfair, doesn’t it? Infelicitous Frank is facing double taxation on his rental income, with both the US and France laying claim to a portion of his earnings.

Thankfully, most countries are parties to DTTs that eliminate the need to pay taxes twice: under the DTT between the US and France, Frank would only have to pay taxes on his rental income once, to France.

So, if you have foreign-source income, be sure to check whether it is subject to taxation in the country of origin. If it is, there may be an exception under the applicable DTT that excuses it from taxation in your tax residence.

4. Double Taxation Treaties (DTTs)

Most countries in the world have entered into DTTs to avoid subjecting income to double taxation. When in doubt about where to pay taxes on a given income source, check the relevant DTT.

As we explored in the previous section, it's not uncommon for a single stream of income to fall under taxation in two countries. However, in many cases, this is seen as unjust, and governments have entered into bilateral and multilateral DTTs to avoid subjecting income to double taxation. In fact, the first DTT was signed back in 1872, when Great Britain and Switzerland agreed to eliminate double taxation of death duties.

Since then, DTTs have proliferated as global economic ties have become increasingly complex and ubiquitous. Currently, there are more than 3,000 bilateral DTTs in effect, and the number is steadily increasing.

Here are the main concepts addressed by modern DTTs.

Double Residency

DTTs provide tie-breaker rules to determine tax residency (whether personal or corporate) in the case that two states can claim taxes from an individual.

Distribution of Taxes

DTTs contain distributive rules that apply to foreign-source income, including from immovable property, dividends, interest, royalty payments, capital gains, and other potential sources. These rules determine whether only one or both of the contracting states can tax the income, and also whether the rate of tax imposed is subject to a limitation.

Elimination of Double Taxation

Generally, there are two methods for eliminating double taxation: the exemption method and the credit method. The rules defining these are usually found at the end of a DTT. In general, if the contracting state in which income arises is entitled to tax the income, the other contracting state (in which the taxpayer is a resident) is obliged to provide relief from double taxation. Under the exemption method, the country of residence excludes or exempts the income from its taxation. Under the credit method, the country of residence taxes the income but provides a deduction for the tax paid on the income to the source country.

Cooperation Provisions

DTTs always provide for some form of administrative cooperation between the contracting states. They also address the exchange of information between the states and term for rendering assistance with tax collection in the other state.

5. Personal Holding Companies

There are plenty of benefits to having a wholly-owned company—some particularly enterprising digital nomads even have several.

Each country has its own set of rules for incorporating, taxing, and regulating legal entities. However, these rules all share a number of common features.

Limited Liability

The great thing about companies is that they let you limit your potential liability and exposure to risk. As a general rule, a shareholder in a company is only liable up to the total amount of their investment in that company. If the company goes bankrupt, the shareholder will only lose their shares in the company, while any personal assets, such as an apartment or car, will not be confiscated.

Corporate Taxation

Companies are taxed very differently than individuals. Corporate taxation can get complicated quickly, but it also offers some important advantages over personal taxation.

Flexibility

You can incorporate a company in any jurisdiction, which gives you the flexibility to select a jurisdiction with laws, a taxation regime, and access to financial institutions that are advantageous to you. In a sense, it’s like a carte blanche for selecting any citizenship you want.

To summarize, doing business via a company provides concrete benefits over submitting taxes as an individual filer, and many digital nomads start their tax planning with setting up a company.

6. Corporate Income Tax

Companies are taxed differently than individuals. This can be leveraged to great advantage by anyone running a business or building wealth.

The more interesting aspects of corporate taxation include the following.

Different Tax Rates

Corporate income is taxed at different rates than individual income. In fact, there are many jurisdictions that choose not to tax corporate income at all.

Pass-Through Entities

Some countries, like the US, have so-called “pass-through entities.” Such entities are not taxed at all. Instead, the income of the entity is treated as the income of the owners. Hence, the owners pay taxes only once, while also enjoying all the benefits of doing business via a company.

Local Income Taxation

Some countries, like Gibraltar, tax only the company’s local income, leaving its foreign-source income untouched.

Taxation of Dividends

To incentivize reinvestment, certain countries with modern tax codes choose to tax only distributed profits, as opposed to earned income. If a shareholder decides not to distribute any dividends and instead reinvests their income into the business or into other assets, no corporate income tax is levied.

Loss Carryforwards

If a company nets a loss in one year, it can deduct that loss from its taxable income the following year. Save for some exceptions, if you as an individual have a bad year and, for example, lose money trading stocks, there is no way to offset taxes on your future profits against that loss.

7. Deductible Expenses

Unlike individuals, companies can deduct business-related expenses to reduce their taxable income, and thus pay less in taxes.

It is a universal tax rule in every jurisdiction that companies pay taxes only on their net income — i.e., on revenue minus business-related expenses (stated in simple terms).

Here are a few examples of business-related expenses that every freelancer or blogger would be well-advised to write off as deductions:

- Furniture

- Software

- Hardware

- Travel

- Hotels

- Coworking-space fees

The governing principle is that expenses must be related to your business for you to deduct them. Buying a fancy cocktail dress may not seem very business-related, but if it’s an essential element in the next viral video to promote your business, it may very well qualify as a business-related expense.

In short, many common expenses can be deducted from revenue to decrease taxable income if you run your business via a company.

Whether something qualifies as a business-related expense can usually be determined using common sense, but it’s always best to consult a qualified accountant for confirmation.

8. Controlled Foreign Companies (CFC)

Companies are an essential instrument in the toolbox of digital nomads, particularly when they’re registered in a favorable jurisdiction.

But governments are, shall we say, rarely overjoyed when their tax residents open offshore companies to reduce their tax burden.

Meet CFC rules.

The concept of CFCs was first introduced in the United States back in 1962. Since then, most developed countries have followed suit and, as of the writing of this article, at least 50 countries have these rules in place. You can check whether CFC rules apply in your home jurisdiction on the OECD website by pressing “Create Table.”

CFC rules tend to be complicated and vary from country to country, but they essentially boil down to this: if you have a foreign company, you need to report that company to the government of your home jurisdiction and pay taxes on any corporate income as if it was your personal income, unless an exemption applies.

Pretty harsh, right? You may wonder why anyone would want to have a foreign company if its income is taxed anyway. Well, there’s a good reason why we wrote “unless an exemption applies” — there are several cases in which this general rule can be avoided. The most common scenarios include:

- Active Company. If the company is actively engaged in business or has “substance” (i.e., is not a shell company) in the foreign jurisdiction, it can avoid CFC rules. Check the qualifying criteria for “active business” and “substance” in your country’s tax code.

- Low Income. If your foreign company is turning a minimal profit, you may be exempted from reporting that income and paying taxes on it.

- Small Shareholding. If you have only a small shareholding in the company, you may fall short of the minimal control threshold to trigger reporting obligations.

Before registering a foreign company, be sure to check the CFC rules of your jurisdiction. Keep in mind that CFC rules in a country usually apply only to tax residents of that country, not to its nationals. This means that (a) you will no longer be subject to the CFC rules of your home country if you lose your tax residency there, and (b) you will be subject to CFC rules of any country where you become a tax resident.

9. Corporate Tax Residence

This sometimes comes as a surprise to aspiring digital nomads, but a company, despite being incorporated in one jurisdiction, may be deemed a tax resident of a different country.

The main criterion to determine the location of a company’s tax residence is its center of management and control. The place where the board of directors meets and makes its decisions is generally regarded as the primary factor in this consideration, but courts may consider other factors as well.

Thus, if you incorporate an offshore company but manage it from your home jurisdiction, the company may be treated as a tax resident of two countries. This is clearly unadvantageous, so it’s essential to determine upfront whether there is a DTT between your home country and the country where your company is to be incorporated. If so, chances are there is a so-called “tie-breaker rule” in the DTT that will specify what happens when a company is deemed to be a tax resident in two jurisdictions.

Most often, a company is a resident of the country where its effective control and management are exercised. It should be noted that some countries have introduced these rules only recently, and there is little precedent or case law on the topic.

Other countries, such as the UK, have a long history of peering through de jure form to examine the substance of corporate control.

To summarize, if you decide to have a foreign company, (a) check if your home country has corporate residency rules and (b) check the applicable DTT.

10. Automatic Exchange of Information

The world economy has been racing down the path of globalization for many years, and tax authorities are doing their utmost to keep pace. Information on foreign taxpayers is readily exchanged between jurisdictions, both by request and automatically.

Paranoid conjectures about a unified world government may be the purview of tinfoil-hat enthusiasts, but the existence of a global tax authority is an undeniable fact — and its influence is growing. Its name: the Organisation for Economic Co-operation and Development (“OECD”).

OECD has been actively developing and promoting a unified framework for cooperation between tax authorities. To date, 141 countries are signatories to the Convention on Mutual Administrative Assistance in Tax Matters, which sets the ground rules on how tax authorities exchange information with one another.

A further 110 countries are signatories to the Multilateral Competent Authority Agreement on Automatic Exchange of Financial Account Information. This agreement lays the framework for automatic exchange of bulk financial information among tax authorities. Under the agreement, the signatories undertake to annually exchange certain information about so-called “reportable persons.”

The information that is exchanged:

- Name, address, taxpayer identification number, date, and place of birth

- Account number

- Name and identifying number of the reporting financial institution

- Account balance or value at the end of the calendar year

- Certain additional information in the case that custodial, depository or other accounts are present

A reportable person is any individual or entity that is tax resident in a reportable jurisdiction as per the laws of that jurisdiction. Reportable persons include individual account holders and controlling persons of accounts opened for legal entities.

Individuals who are dual residents should reference the tie-breaker rules contained in their relevant DTT to determine the location of their tax residence.

The automatic exchange agreement was signed into action in 2015. Notably, the US is not yet a signatory to the agreement, which means that they do not automatically exchange information with other countries on foreign taxpayers holding American accounts.

This is it. We hope this guide will help you navigate international tax laws when you move to your ideal location. If you have any further questions, please feel free to contact the authors.

Contacts

.svg)

.svg)

.svg)

New York, NY 10003-1502